Recognizing and understanding the Cost of Debt is vitally important for any company or individual who relies on debt financing. Simply put, debt costs refers to any expense incurred from borrowing money - from interest payments and associated fees through to decisions which could significantly impact financial outcomes and decisions.

By being aware of their own debt costs and ways to calculate and minimize them effectively, entities can better manage their finances, increasing their potential profit and stability in competitive environments.

Understand the Cost of Debt

Definition and Importance

The cost of debt refers to the effective interest rate that a company pays on borrowed funds, such as bonds, loans or lines of credit.

It plays a key role in business strategy and financial planning decisions as it impacts decisions regarding financing and capital structure decisions - for instance how companies balance debt vs equity finance to maximize financial health while optimizing operational performance and minimize costs while optimizing operational efficiency.

A lower cost of debt indicates less costly borrowing that can increase profitability while providing greater flexibility with financial decisions.

Factors Affecting Debt Payments

Numerous factors influence the cost of debt for businesses. These include:

- Creditworthiness: Companies with higher credit ratings often qualify for lower interest rates on debt due to being perceived by lenders as lower risk.

- Market Conditions: Current economic factors such as inflation rates and economic cycles impact lending rates set by banks and financial institutions.

- Loan Terms: Both the length and amount borrowed can influence the interest rate offered on loans, with longer loans or larger amounts typically carrying greater risks and incurring higher rates as a result.

- Types of Debt: Different forms of debt such as bonds, bank loans or debentures come with various costs based on their inherent risk and maturity structures.

By understanding these factors, companies can develop strategies to secure financing at more favorable rates and reduce their overall debt costs.

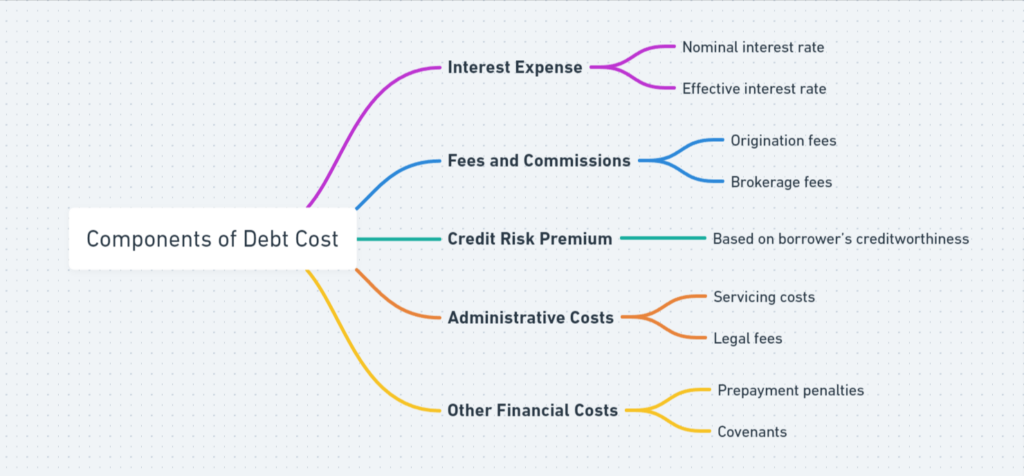

Components of Debt Cost

Interest Rates

Interest rates are an essential element of debt repayment costs, representing the percentage of principal a borrower owes over and above their principal repayment obligation to lenders as interest.

They tend to be determined by benchmark interest rates set by central banks as well as the specific terms of a business's loan agreement and may either remain static over its life or fluctuate based on market fluctuations.

Fees and Charges

Businesses should take note of various fees and charges which add up to the total cost of debt, in addition to interest rates. Examples may include:

- Origination Fees: Costs associated with initiating new debt.

- Closing Costs: Administrative fees that must be paid when closing on a borrowing transaction.

- Prepayment Penalties: Any fees assessed against early repayment of debt.

Calculating the true expense of borrowing requires taking these fees into account in your calculations.

Other Considerations Whilst Assessing Debt

Other considerations must also be kept in mind when calculating the cost of debt, including interest rates and fees, including:

- Tax Implications: Interest expenses can often be deducted, which helps lower the net cost of debt.

- Impact on Credit Rating: Accumulated debt can negatively impact a company's credit rating and cause future borrowing costs to increase, impacting future costs of borrowing as a result.

Considerations of all these aspects can provide businesses with a more complete picture of the costs associated with debt, enabling more informed financial decisions to be made.

Influence of Debt Cost on Financial Decisions

Understanding the cost of debt is of utmost importance in many different financial decisions across sectors such as businesses, individuals and investment strategies.

How it's managed can have serious ramifications on profitability, financial health and the overall strategy of an organization or individual.

Businesses

Debt costs play an integral part of financial structures for businesses. Excessive interest charges on borrowed funds can result in higher debt service costs that eat into profitability, prompting business executives to carefully consider debt costs when financing projects, expansions or acquisitions.

Lower cost debt allows a company to access necessary capital without severely disrupting cash flows - making strategic moves more viable overall. Furthermore, tax implications often reduce net costs of debt significantly.

Individuals Debt costs have an immense effect on individual finances and purchasing power. Mortgage, car loan, credit card debt or student loan decisions all depend upon debt costs incurred; lower cost means more manageable monthly payments and overall debt load which increases savings and investing opportunities, while high debt costs restrict budgets and limit growth potential.

Investments

Investors must also carefully consider the cost of debt when considering potential investments. When purchasing real estate, decision-makers often rely on mortgage rates; lower mortgage rates make investments more appealing as they reduce borrowing costs and enhance returns.

Corporate bonds or other fixed-income instruments are evaluated on interest expenses; investments that charge high rates of interest tend to be less desirable investments.

Calculating Debt Costs

Accurate financial analysis and sound decision-making require accurate calculations of debt costs, which involve several key components and assumptions which need to be carefully taken into account during this process.

Formulas and Methods

The basic formula for calculating debt (Kd) is I/P; where I represents annual interest expense and P is principal amount or loan face value.

To get more accurate results, it's also necessary to adjust this formula for tax consequences as most interest payments can be deducted against tax liabilities; an adjusted formula would then become Kd = I(1-Tc)/P; thus providing a post-tax cost of debt more representative of its actual financial impact on a company.

Practical Examples

Let's assume a company has taken out a loan of $100,000 with an annual interest rate of 5% and corporate tax rate of 30%; their annual interest expense would amount to $5,000 using the post-tax cost of debt formula.

Kd = $5,000 (1-0.30)/ $100,000, which equals $3,500 divided by 100,000 and divided by 35% to get 3.5% as the Kd value. Understanding this rate, which reflects tax benefits of debt, is integral for making informed financial decisions.

For instance, someone taking out a non-tax-deductible personal loan at a 7% interest rate with the same principal amount pays a cost of debt equaling that interest rate without any tax relief relief - an illustration that makes clearer how various financial scenarios impact debt costs.

Effective Debt Management

Achieve maximum profitability and financial health requires businesses to properly manage the costs associated with debt. This involves understanding current loans' terms and monitoring market conditions for better opportunities while taking steps to minimize overall expenses associated with borrowing money.

Strategies to Cut Costs Effectively

Companies seeking to reduce debt costs must employ multiple strategies in order to do so, including:

- Negotiate for Lower Interest Rates: Engage lenders in order to decrease the interest rates on current loans and directly lower costs associated with interest expenses.

- Opting for fixed rates: Instead of variable ones can help protect costs from rising in response to interest rate fluctuations and provide more predictable financial planning.

- Strengthen Creditworthiness: By upholding strong credit, businesses can qualify for loans with more favorable terms, including lower interest rates.

- Timing the Market: Refinancing or taking on new debt when interest rates are at their lowest will take advantage of lower borrowing costs available in financial markets.

Refinancing and Debt Consolidation Solutions Available Now

Refinancing involves swapping out existing debt with new loan with lower interest rate, while debt consolidation combines multiple loans into one with potentially reduced average interest rates.

Both strategies can simplify financial obligations and bring significant cost savings - benefits of these approaches include:

- Refinancing can significantly lower interest payments over the life of your debt.

- Consolidation helps manage debt by consolidating multiple payments into one monthly schedule with potentially lower cumulative interest.

- Refinancing may also extend the repayment period and decrease monthly payments, while increasing total interest over time.

Refinancing and debt consolidation are key ways for businesses to create more manageable and cost-effective debt structures.

Book a Demo and experience ContextQA testing tool in action with a complimentary, no-obligation session tailored to your business needs.

Conclusion

Debt cost analysis is an integral component of business analysis that allows companies to understand the true expense of borrowing.

Understanding its true expense allows businesses to make informed decisions when considering debt as a tool for organizational expansion; lower rates indicate more affordable debt service while higher ones indicate riskier ventures.

Organizations should aim to optimize their capital structure so as to align its cost of debt with strategic financial goals for maximum financial and operational effectiveness.

Also Read - The Importance of Different Layers of Testing in Software Development